It’s an uncomfortable truth that the right answer to big questions in marketing strategy is nearly always “it depends”.

What should the brand vs activation mix be? It depends. Which media channels have the strongest return on investment? It depends. And on the question of the moment: How much should I spend on media during the coronavirus recession? It depends.

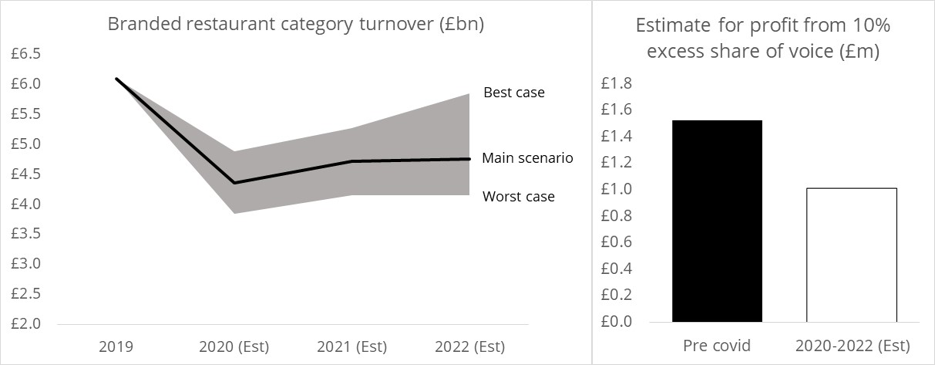

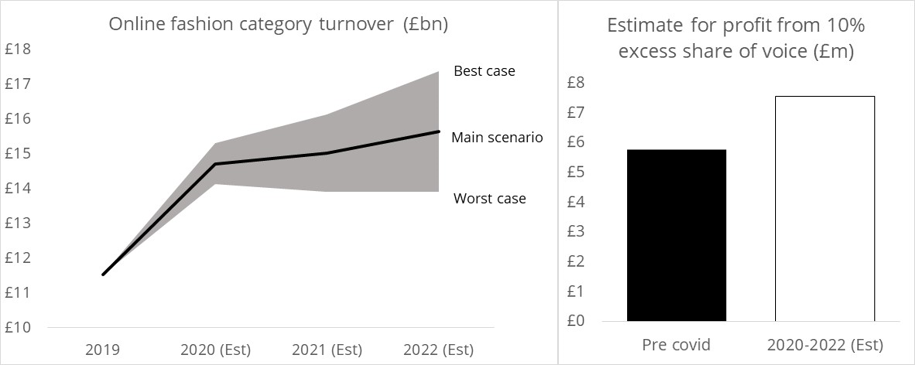

The thing it depends most on is the health of your category. If you invest during a recession you can get cheap share of voice, which over time will bring increased share of market.

But whether that additional market share is worth it depends on how big your category is during and after the recovery. Buying a larger share of a category that continues to struggle might not pay back – even in the long term.

So far, different categories are experiencing very different crises because of the practicalities of lockdown and social distancing. Sectors that involve in-person interactions – education, hotels, restaurants, and construction – are all down by more than 70% in Q2. Agriculture, where people work alone outside, and financial services, where people can easily work from home, are broadly unaffected.

But the outlook as the crisis recedes is equally important for the decision about investment now. Different categories will be very different on this too, and there are three reasons why.

First is the extent of knock on effects, particularly reduced demand from newly unemployed or insecure workers. This is likely to be damaging in categories where purchases are a treat rather than a necessity. And it is particularly detrimental wherever the target market is under 30 years old or in low income jobs because these are the demographics most affected by redundancies and wage cuts.

Second, and pulling in the other direction, some categories will see a growth spurt driven by pent-up demand. This will likely benefit manufacturing and retail categories where purchases can be delayed. But service categories won’t see the same benefit; however many haircuts we miss, we’ll only need one when lockdown is over.

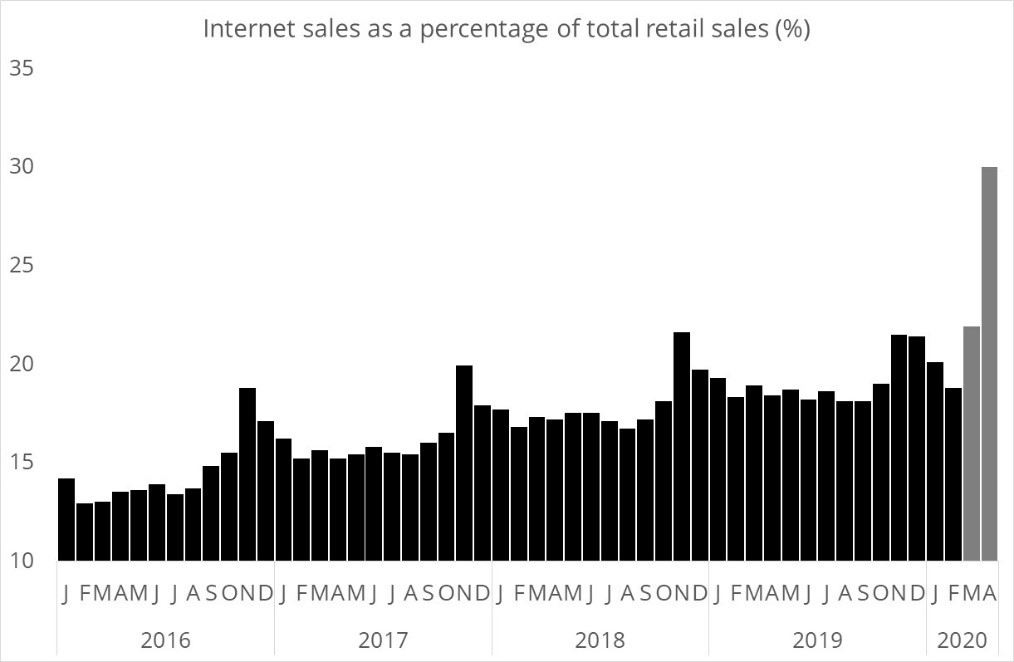

Finally, there’s the question of in person vs online shopping. During lockdowns a much larger proportion of shopping is taking place online, and based on past experience it’s likely that ecommerce categories will emerge stronger from covid 19 too.